Kamakura Releases Seventh Generation Public Firm Default Probability Models

KRIS 7.0 Based on 5 Years of Daily Cross-Validation Using Traded Bond Prices

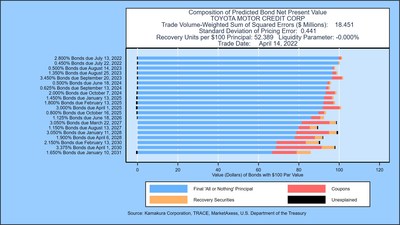

NEW YORK, April 19, 2022 /PRNewswire/ — Kamakura Corporation reported Tuesday that the seventh generation of Kamakura public firm default models is being rolled out to central banks, regulatory agencies, banks, insurance firms, fund managers and government clients world-wide. The seventh-generation models, the Kamakura Risk Information Services (“KRIS”) version 7.0 models, include the state-of-the-art Jarrow-Chava reduced form model, a modern econometric implementation of the Merton model, and a Jarrow-Merton hybrid model in the reduced form model framework. The models were benchmarked on more than 4.3 million observations from 24 countries. The KRIS 7.0 models mark the 20th anniversary of first KRIS models released in 2002. Version 7.0, which has been in development since 2017, reflects a daily out-of-sample cross-validation using traded bond prices and the Hilscher, Jarrow and van Deventer reduced form bond model.

Kamakura Corporation founder and chief executive officer Dr. Donald R. van Deventer explained the innovations behind the KRIS 7.0 modeling effort. “Three key analytical strategies are reflected in the KRIS 7.0 models: cross-validation using bond prices, Bayesian insights, and a rigorous missing data modelling process. The Hilscher, Jarrow and van Deventer ‘HJV’ model allows Kamakura to test default models not only on binary default/no default flags but also on traded bond prices. In addition, the HJV model allows Kamakura to extract fully compatible recovery rates and liquidity parameters for excellent accuracy in fitting traded bond prices. Professor Jarrow’s 28 years at Kamakura Corporation have had a very significant impact on the KRIS 7.0 models. The Bayesian insights reflected in the model can be seen both in the development path and in the second-stage empirical Bayes coefficients that are an important companion model to the KRIS 7.0 models that are first to be released. Finally, missing data in the KRIS models has taken on the same significance as missing witnesses and missing evidence in the law enforcement process. Missing data can and does have significant incremental explanatory power in the KRIS 7.0 models.”

Martin Zorn, president and chief operating officer of Kamakura Corporation, commented “The KRIS 7.0 models continue to demonstrate that high leverage and rapid movements in important macro factors drive public firm default around the world. The rich history of default probabilities for 40,500 firms in KRIS allows for a very high-quality ability to simulate default probabilities forward as a function of the macro-economic environment. A supplemental subscription to the KRIS Macro Factor Service provides a sophisticated econometric relationship between fully disclosed macro factors and historical default probabilities for each combination of firm, default model, and default probability maturity. All coefficients are disclosed, as are performance measures and full documentation of the reduced form credit portfolio simulation technology. These forward-looking econometric relationships perform a dual role as state-of-the-art best practice models for simulation and stress testing and as challenger models for in-house models developed using internal data by large institutions.”

The KRIS version 7.0 models were developed using a data base of more than 4.3 million observations and more than 4,100 corporate failures in 24 countries. A complete technical guide is provided to subscribers which includes full model test results and parameters. The KRIS service also includes a wide array of other default probability models that can be seamlessly loaded into Kamakura’s state of the art enterprise risk management software engine Kamakura Risk Manager. Models available include the non-public firm default model, the U.S. bank model, and the sovereign model. Related data includes market implied credit spreads and prices on all corporate bonds traded in the United States market. Macro factor parameter subscriptions include Heath, Jarrow and Morton term structure models for government securities in the United States, Canada, France, Germany, Italy, Russia, Spain, Sweden, the United Kingdom, Australia, Japan, Singapore, and Thailand. Kamakura also offers a very powerful World model consistent with empirical Bayes insights. All parameters are derived in a no-arbitrage manner consistent with the seminal papers by Heath, Jarrow and Morton and Amin and Jarrow. A KRIS Macro Factor Scenario Service subscription includes both risk-neutral and “real world” empirical scenarios for interest rates and macro factors.

About Kamakura Corporation

Founded in 1990, Honolulu-based Kamakura Corporation is a leading provider of risk management information, processing, and software. Kamakura was recognized as a category leader in the Chartis Report, Technology Solutions for Credit Risk 2.0 2018. Kamakura was named to the World Finance 100 by the editor and readers of World Finance magazine in 2017, 2016 and 2012. In 2010, Kamakura was the only vendor to win two Credit Magazine innovation awards., Kamakura Risk Manager, first sold commercially in 1993 and now in version 10.1, is the first enterprise risk management system for users focused on credit risk, asset and liability management, market risk, stress testing, liquidity risk, counterparty credit risk, and capital allocation from a single software solution. The KRIS public firm default service was launched in 2002. The KRIS sovereign default service, the world’s first, was launched in 2008, and the KRIS non-public firm default service was offered beginning in 2011. Kamakura added its U.S. Bank default probability service in 2014.

Kamakura has served more than 330 clients with assets ranging in size from $1.5 billion to $9 trillion. Current clients have a combined “total assets” or “assets under management” in excess of $38 trillion. Its risk management products are currently used in 47 countries, including the United States, Canada, Germany, the Netherlands, France, Austria, Switzerland, the United Kingdom, Russia, Ukraine, South Africa, Australia, China, Hong Kong, India, Indonesia, Japan, Korea, Malaysia, Singapore, Sri Lanka, Taiwan, Thailand, Vietnam, and many other countries in Asia, Europe and the Middle East.

To follow risk commentary by Kamakura on a daily basis, please follow:

Kamakura CEO, Dr. Donald van Deventer (www.twitter.com/dvandeventer)

Kamakura President, Martin Zorn (www.twitter.com/riskmgrhi)

Kamakura’s official twitter account (www.twitter.com/KamakuraCo).

For more information, please contact:

Kamakura Corporation

2222 Kalakaua Avenue, Suite 1400, Honolulu, Hawaii 96815

Telephone: 1-808-791-9888

Facsimile: 1-808-791-9898

Information: [email protected]

Web site: www.kamakuraco.com

Photo – https://mma.prnewswire.com/media/1799351/KRIS_Cross_validation_Using_Bond_Prices.jpg

Logo – https://mma.prnewswire.com/media/657972/Kamakura_Logo.jpg